Germany’s dairy market report

The three public authorities in Germany (Federal Agency for Agriculture and Food), in Austria (Agrarmarkt Austria) and in France (FranceAgriMer) have jointly analysed the markets for milk in 2017. The aim of this analysis is to describe, how Germany, Austria and France have been affected by the events in 2017 and to explain specific trends in the respective three countries.

This report describes the main events and developments in 2017 in terms of milk deliveries, producer milk prices and the production of dairy products (butter, skimmed milk powder, cheese) in the conventional as well as in the organic sector.

The joint report was marked by three things: the recovery of producer milk prices in most member states of the EU and especially in Germany, France and Austria, the increase in milk deliveries in the European Union (from March in Austria, but a little later in the two largest milk producing countries Germany and France) and the valuation difference between milk fat and protein, which recorded a historic high: While the shortage of butter drove prices up in response to dynamic global demand, the 376,000 tons of skimmed-milk powder stored by the EU had a burdensome effect, with prices below the intervention price.

In Germany, in June 2016, the price of conventionally produced cow’s milk reached a long-standing low in Germany. For the first time the German delivery volume was lower than in the same month of the previous year. From this time on also in the year 2017 the deliveries decreased compared to the previous year.

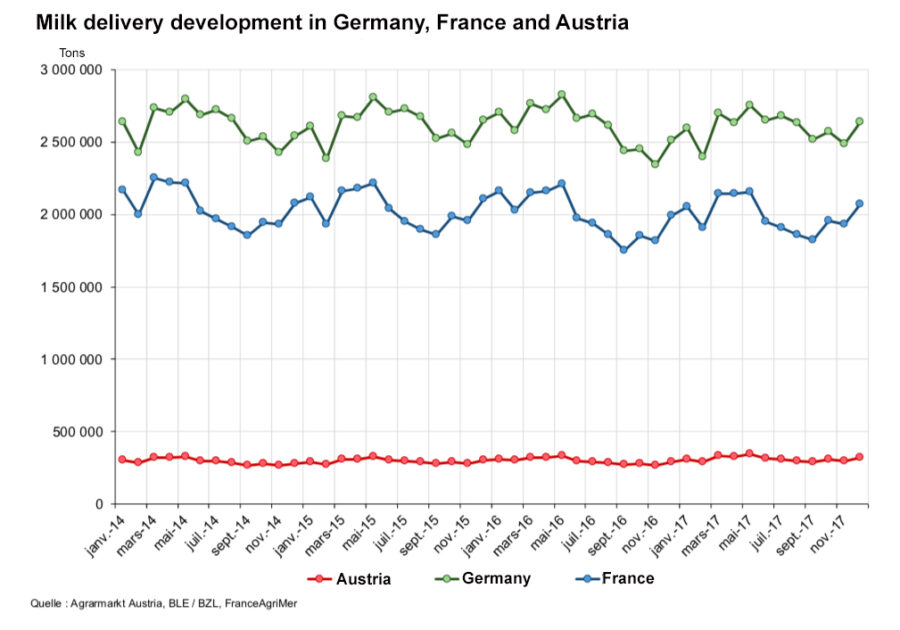

Milk deliveries by German and European producers to German dairy companies for 2017 amounted to 31.9 million tons, which was 0.1% below the level of 2016. German dairy producers’ milk deliveries declined by 0.2% compared to the previous year.

A special measure to decrease production showed only a temporary effect. After the end of the retention period, from June 2017 onwards, there was a further increase in milk deliveries compared to the previous year, which began in northern Germany (Lower Saxony and Schleswig-Holstein) and spread south and then east.

Last year 7.7 million tons of cow’s milk were delivered in Bavaria, the largest amount. Producers from Bavaria, Lower Saxony and North Rhine-Westphalia, the three federal states with the largest delivery volumes, together delivered 17.8 million tons of milk to the dairy companies in 2017. The share of these three federal states in the total supply of German producers thus corresponds to 56.8%.

Reduction in milk delivery is also due to the lower number of dairy cows. Between November 2015 and November 2016, the number of dairy cows decreased by 1.6% and in November 2017 a further 0.4% less cows (-18,690 dairy cows) were counted.

32.7 million tons of cow’s milk was produced in Germany in 2017. 31.3 million tons were supplied to dairy companies. The average milk yield per cow and year in Germany changed from 7,746 kg in 2016 to 7,780 kg in 2017.

In 2017, the delivery of foreign producers to German dairies amounted to 681,895 tons, which was 2% of total delivery volume.

While the volume in 2017 of conventionally produced cow’s milk delivered to dairy companies in Germany almost equalled the volume delivered in the previous year, more organic milk was delivered, +18.2%, than in the previous year. In 2017 around 3% of the total delivered cow’s milk was produced organically/biologically (2016: 2.5%). In contrast to conventionally produced cow’s milk, organic milk increased by double digits in all months of 2017 compared to the same months of the previous year.

With 22.46 cents/kilogram in average in June 2016, the milk price in Germany reached an extremely low level. With the reduction in German milk deliveries in June 2016 below the level of the previous year and the supply shortage in the EU a price increase for conventionally produced milk occurred. The monthly cash price for conventionally produced cow’s milk rose in January 2017 to 32.53 cents/kg and it peaked in October (39.41 cents/kg). The milk price was supported by the relatively high prices for milk fat. With the fall in butter prices in October and rising milk deliveries, the price of milk fell slightly to 38.46 cents/kg by December 2017. This downward movement continued until April 2018 (35.51 cents/kg).

The annual average price for 2017 was 36.19 cents/kg, which was 9.46 cents, or 35.4% above the previous year’s price.

The prices for organic milk are at a significantly higher level than the prices for conventionally produced cow’s milk and in Germany they remain just under 50 cents/kg and were also very stable in 2017.

Arounf 4.7% less drinking milk (4,743,000 tons) was produced in 2017 compared to the previous year. A slight decline in drinking milk production is also observed for the year 2018. The main reason is the lower demand in the retail sector, as consumer milk had significantly increased in 2017 compared to the previous year. Whole milk (2,464,100 tons) and semi-skimmed milk (2,015,400 tons) accounted for the largest share of total production in 2017.

The production of butter, including dairy fat and dairy fat products, decreased by 3.6% in 2017 to 496,900 tons. Brand butter accounts for the largest share.

Butter competed with fatty cheeses and yogurt products for milk fat. Prices for 25kg of block butter increased from € 4.08/kg to 7.04/kg in February 2017 due to high demand from February on and the prices for 250g packets would follow the same trend one month later.

Production of German cheese, including processed cheese and processed cheese preparations, reached a high level in 2017 at 2,480,700 tons.

The cheeses, with a fat content of 45% or more in dry matter, accounted for the largest share, at just under 1.3 million tons. With 31.9% of total production or 791,400 tons cream cheese in 2017 continued to account for a large share of cheese production. Due to the lower production volumes of cream cheese compared to the previous year (-2.9%), cheese production decreased by 0.7% in 2017.

Total German imports of cheese increased in 2017 compared to the previous year to 847,500 tons (+2.9%) and exports to 1,220,200 tons (+4.5%).

In Germany, 430,400 tonnes of skimmed milk powder were produced in 2017. The production fluctuated between 37,000 and 34,000 tons per month, only in December 2017 it rose to over 41,000 tons to cope with the high milk-fall over the Christmas holidays.

In the first half of 2017, skimmed milk powder production was down on the previous year and in the second half. Overall, production fell by 1.2% year-on-year.

By the beginning of 2017 skimmed-milk powder in public storage 58,842 tonnes was in Germany. As a result of further purchases, which were significantly lower than in the previous year, skimmed milk powder stocks increased to 65,571 tons in Germany (378,000 tonnes in all EU).

By contrast, private storage stocks in Germany decreased from 13,780 tons of skimmed milk powder in January 2017 to 723 tonnes in December.

In 2018 (as of May) 17,856 tons has been sold (at varying prices between €105 and €127).

While German imports of skimmed milk powder were 64,000 tons, the export increased by 11% to nearly 400,000 tons, or more than 90% of production.

The importance of the organic dairy market is increasing in Germany, but based on a relatively low starting level. The largest increase in 2017 compared to the previous year was the organic butter production increasing by 15% to almost 16,000 tons. Drinking milk accounted for the largest production volumes of 354,000 tons (+6%), while organic cheese grew by just under 10% to around 47,000 tons compared to the previous year.